Returning to America and the (Un)Affordable Care Act

I worked in the American health insurance industry during the original Affordable Health Care (ACA) debates back around 2009. I watched a lot of money spent on completely wasteful projects as the entire industry lobbied against a public single-payer option. In January of 2016, I returned to the States after being outside the country for four years. I hadn’t been required to obtain insurance via the ACA while living outside the US. When I looked at my options upon returning, I discovered that many of the fears concerning the Affordable Care Act had proven to be true. All my current options for health coverage, both via my employer and the ACA, either leave me paying more than I ever have in my life for terrible coverage, or paying very little for preventative only care.

When I returned to the US, I took a contract job via a staffing company. Upon hire, I looked at my benefits and, at first, was surprised how affordable they were. I was only paying $14.30 for health and $7.94 for dental per paid period (weekly). However, the health care only included preventative. It was a minimal effective coverage plan, meaning it barely met the requirements of the affordable care act. After a few months, open enrollment began and I was given the option to subscribe to full Preferred Provider Organization (PPO) plans. The cheapest individual plan was over $400 per month.

Paying obscene amounts of money for health coverage from staffing companies is not unheard of. Conversely, full-time employers often subsidize health insurance plans to incentivize potential hires. The previous highest rate I’ve paid for health insurance was approximately $200 per month, also via a small staffing company in Cincinnati. At the time it was presented before me, I even said to the staffing agent, “This is more than I’ve ever paid for health coverage in my life.” Thankfully I was able to find another position a few months afterwards.

I decided to look at the ACA plans offered to see if I could find something more affordable. A state can offer their own marketplace, or defer to using the federal government running their market1. The state of Washington runs their own marketplace. During their open enrollment period, I attempted to find a health plan. The first issue was that the Washington Health Plan Finder website was terribly designed and buggy.

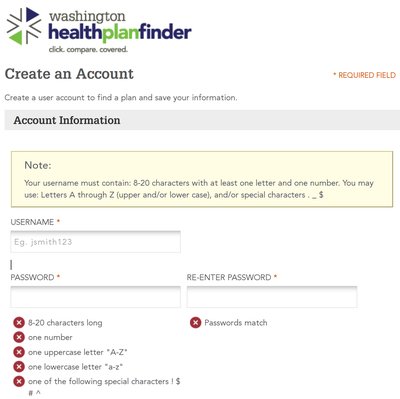

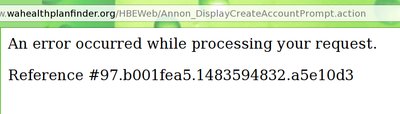

The password requirements alone didn’t fit any of my password algorithms, and I could not validate my password even thought it met all the requirements. Eventually I discovered a bug where the site would not accept some of the special characters it has listed. During the account creation process I ran into other errors that left me frustrated. The number of bugs I encountered makes me question the security of the Health Plan Finder website and whether it should even be trusted with my personal information.

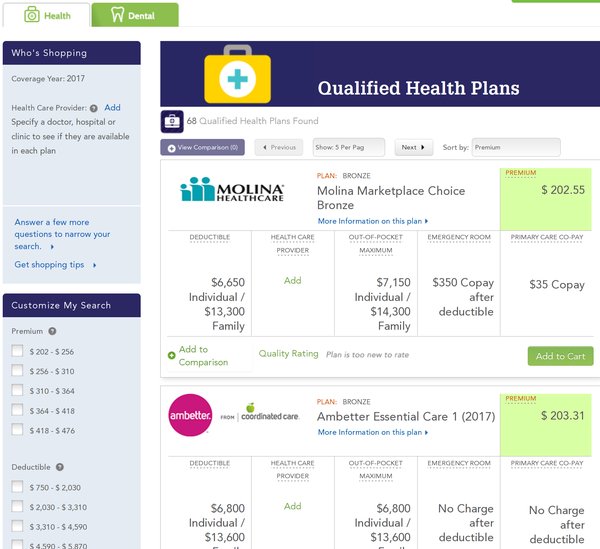

After I finally created an account, I had to enter in all my income and tax information. It essentially requires a miniature version of your income taxes in order to operate. After entering all my information, the following were the lowest price plans I was offered:

The cheapest premium was $202.55, with a $6,650 deductible. Although there is a $35 co-pay for doctors visits, in my experience when I had a high debatable plans combined with a health savings account (HSA), doctor’s visits were around $200 ~ $250 for walk in clinics, as an entirely out-of-pocket expense. During times when I was unemployed and called around asking for rates. Some health providers would offer more reasonable rates, which I could pay for with my previous HSA.

For comparison, while I was overseas in Australia and New Zealand, where I had no insurance, I never paid over $75 (in their respective currencies) for a general practitioner (GP) visit. While I was in Melbourne, there were even protests against the Abbot government for wanting to impose a $7 co-pay for doctors visits2. At the time, Australians weren’t charged anything for simply seeing a GP.

The Working Poor

The ACA was not for people like me, or really anyone in the middle class with employer sponsored health care. It has brought affordable health care, in some states, to people above the absolute poor, who previously didn’t have access to any type of coverage. Self employed nannies, caretakers and other people in low income or self-employed service positions can potentially find affordable coverage under ACA plans.

Affordable care act plans are also inconsistent between states. In 2016, Arizona only had two health insurance companies that offered health plans on the public marketplace, with Blue Cross Blue Shield of Arizona increasing their ACA premiums by 51%. In Maricopa County, only the single option of Centene Corp remains, which was allowed a 74.5% premium increase by state regulators3.

Throw the Whole Thing Out

The Affordable Care Act is colloquially referred to as Obamacare, even though much of the ACA is based off the Massachusetts health care plan, colloquially refereed to as Romneycare. There is a lot of emotional attachment to the ACA, mainly by people who have never had to use it; people who rely on their employer’s health care plans. Although some people have benefited, many are now required to purchase private health care, that have high deductibles and questionable coverage, or face additional IRS tax burdens.

The absolute poor have always had coverage in America, simply because they cannot afford any doctors bills that are issued to them4. Their debt is often written off by hospitals. The ACA added the income bracket above the absolute poor to get some kind of meaningful coverage, but unfortunately that coverage hasn’t been consistent across America and it hasn’t helped the middle class who still depend primarily on employer sponsored plans.

There are fears that Trump will repeal Obamacare and replace it with Trumpcare. There are very few details about what President Trump intends to offer in a health proposal, other than removing the restrictions baring insurers from selling across state lines. As with the original health care debate, whatever changes his administration plans to make will mostly likely just place more money in the hands of the private health care sector, making an already flawed system increasingly irrelevant. I also think that had McCain or Romney created the current ACA, those solidly in the left/liberal base would adamantly oppose the current health care structure, with their anger arising from the false left/right paradigm.

“If you like the plan you have, you can keep it. If you like the doctor you have, you can keep your doctor, too.” -President Obama5

Obama’s promise that people could keep their existing employer based health care plans was probably the largest detriment to any real health care reform. At a minimum, marketplace plans needed to be substantially better, leading people away from employer based plans, for the ACA to have any real effect. The alternative was the proposal for a single payer system. Every citizen should have been covered, using existing taxes, and should not have been forced to buy private insurance from the horribly corrupt and terribly inefficient, for-profit or not-for-profit health care industry. The private sector would not go away, but instead, a public option would have most likely be contracted out to the same private companies, in the same way Medicare is currently run.

The Problems are Systemic

During my time in the health insurance industry, I worked closely with several people who worked on the Medicare side of coverage. Even though there were complaints from customer service representatives about how the government didn’t give them enough to pay doctors, the insurer still did find a way to negotiate, pay providers, and cover the insurers expenses within the existing framework. The set Medicare rates are good enough, and replacing private insurance entirely would mean those companies would have to cut their inefficiency in order to survive.

Advertising, lobbying and other superfluous programs would need drastic cuts. Many companies would have large reductions of force, resulting in layoffs and redundancies. This may seem like a negative, but many of the positions that would be cut are skilled positions; people who can find other work.

What would take more time is fixing all the other hidden costs within the industry. Clinics and hospitals are under constant pressure from staff (physicians, nurses and lab technicians) to provide them a high income. That high income is often needed to pay off the increasing amounts of debt from student loans and higher education. Any viable solutions for health care would need to tackle all parts of this human resource supply chain, and include better grants and scholarships for doctors, reduction of education cost and reduction of lobbing and bloat within the pharmaceutical, hospital and medical school industries. The problem space is large, because the causes are systemic. They grew gradually over time, like a bacteria infecting a body. In America, we’re in a state where we cannot cure the host, but instead must keep the organism alive while also keeping alive the infection that is killing it.

Removing the bloat from the industry will be painful, but if done correctly, it will be like ripping off an adhesive bandage. This type of reform would not be popular at first. Any political candidate who implemented it, would most likely not get reelected. The long term benefits would take time to manifest themselves, but the result could be immensely meaningful to countless US Citizens and residents.

We Must Always Work, Endlessly, For Our Health

In the United States, citizens are in a reality, where we continually have to work. Breaks and sabbaticals from employment means the negation of health coverage for individuals. Those with partners or those under 26 years of age may have options of dependent coverage, but for everyone else, health care helps to server the same function that student loan debt has come to server. It keeps people tied to relentless work, without respite.

For those with lower incomes, it is another barrier to moving up the social ladder. Too much income can result in loss of affordable coverage, if one is lucky enough to live in a state that even offers such plans. For individuals that are self employed in the service economy, this could prevent them from growing businesses or taking more clients for fear of losing coverage. Moving within these brackets often requires the loss of autonomy and jumping to a full-time position in a larger company that offers affordable options.

The way healthcare is structured in America is absolutely staggering. The current structure came about through a combination of negligence, lobbying and outright malice. The original intent of the private health care industry may not have been to keep people trapped in the human resource factory framework. Yet in its current form, it is another piece of the system of controls which keep Americans attached to jobs and careers until they are only enough to qualify to Medicare. It’s evolved into another means to keep Americans working until they are either too old or too disabled to be of any use.

-

A US Health Care System Primer for Non-US People. 17 Jan 2017. Don Jones. ↩

-

Tony Abbott moves to plan B on Medicare co-payment for GP visits. 8 Dec 2014. Taylor and Hurst. The Guardian. ↩

-

‘Obamacare’ in Arizona: 2 remaining insurers hike rates by 50-75 percent. 25 Oct 2016. Alltucker. AZ Central. ↩

-

HOSP-ITALITY ABUSE. 12 July, 2009. Otis. New York Post. ↩

-

WEEKLY ADDRESS: President Obama Outlines Goals for Health Care Reform. 5 June 2009. Whitehouse.gov Archives. ↩